Designating Retirement Plan Beneficiaries

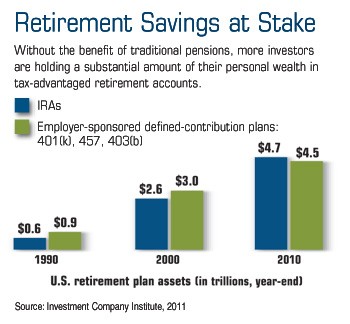

IRAs and defined-contribution plans have become an important component of personal wealth — averaging roughly 60% of the assets of U.S. households with $100,000 or more to invest, according to recent research.1

IRAs and defined-contribution plans have become an important component of personal wealth — averaging roughly 60% of the assets of U.S. households with $100,000 or more to invest, according to recent research.1

Designating account beneficiaries (in light of your overall estate conservation strategy) and keeping those designations up to date can be a complex process, especially if you have been married more than once. It may not be wise to assume that your survivors would honor your spoken intentions in the event of a mistake or oversight.

The beneficiaries you designate and varied retirement plan rules typically supersede instructions in your will; therefore, a beneficiary form could easily become one of your most crucial estate conservation documents.

Plans Play by Different Rules

Some individuals may not know that a will does not control who will inherit retirement plan assets, or they may simply forget to make desired changes in writing. For example, an account holder who is divorced may intend to leave retirement plan assets to his or her children. But a former spouse could receive the money if the account beneficiary form was never updated, even if a will and a divorce decree state otherwise.

If no beneficiary is named — or the designated person is deceased and there is no secondary beneficiary — retirement assets may be transferred according to the administrator’s plan documents rather than an account owners preferences.

There also may be a significant difference in the government rules that apply to employer-sponsored plans and some IRAs. Federal law requires that spouses automatically inherit assets held in workplace plans such as a 401(k), unless the spouse signs a waiver allowing the participant to designate someone else. IRAs, on the other hand, are subject to laws that vary from state to state; spousal waivers may or may not be necessary.

There also may be a significant difference in the government rules that apply to employer-sponsored plans and some IRAs. Federal law requires that spouses automatically inherit assets held in workplace plans such as a 401(k), unless the spouse signs a waiver allowing the participant to designate someone else. IRAs, on the other hand, are subject to laws that vary from state to state; spousal waivers may or may not be necessary.

In one case, a man who died unexpectedly six weeks after a second marriage accidentally disinherited his children. Courts awarded his employer-plan assets to the new wife — even though his children were the designated beneficiaries — because the wife had not waived her rights to the plan assets.2

A Few Things to Remember

- Many laws favor spouses, so be careful when you intend to name someone other than your spouse as a beneficiary.

- Don’t name minor children without making arrangements for a guardian or trustee to control the assets until the beneficiary is old enough to manage them.

- Review your beneficiary designations annually, and inform your financial professional when there are changes in your life that could affect your choices, such as the birth of a child, the illness or death of a beneficiary, marriage, divorce, and especially remarriage.

- Keep in mind that beneficiary designations usually don’t carry over when you roll 401(k) assets to a new employer’s plan or to an IRA, or if you convert a traditional IRA to a Roth IRA.

- Request an acknowledged copy of each new or updated beneficiary form from the financial institution or your financial professional and store them with your other important documents.

Distributions from traditional IRAs and most employer-sponsored retirement plans are taxed as ordinary income. Withdrawals taken prior to age 59½ may be subject to a 10% federal income tax penalty, with certain exceptions such as death and disability. Employer-plan distributions may be penalty-free following separation from service at age 55 or older. IRA distributions may be penalty-free if used for qualified higher-education expenses or a first-time home purchase ($10,000 lifetime maximum).

1–2) The Wall Street Journal, September 7, 2011

The information in this article is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax or legal advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Emerald. Copyright © 2012 Emerald Connect, Inc.